Federal estate tax and the 2026 changes: what Raleigh high earners need to know

If you’re a physician, business owner, or executive in Raleigh earning $300,000 or more per year, the federal estate tax landscape just changed significantly. The sunset that had estate planning attorneys across the country scrambling? It’s gone. But that doesn’t mean the planning conversation is over.

This page walks you through exactly what changed, what the current federal estate tax exemption means for your family, and why the elimination of the sunset provision creates a different kind of planning opportunity for high-income North Carolina professionals.

On this page:

• What is the federal estate tax exemption in 2026 and how does it affect Raleigh high earners?

• Do high income earners in Raleigh, North Carolina owe state estate tax?

• How will the 2026 federal estate tax changes affect Raleigh high income earners?

• What happens if the exemption drops in the future?

• Frequently asked questions

At a glance:

• The federal estate tax exemption increased to $15 million per individual ($30 million for married couples) for 2026, and this higher threshold has no scheduled sunset under the OBBBA.

• North Carolina residents face no state estate or inheritance tax, meaning the federal exemption is the only estate tax threshold that applies.

• The TCJA sunset that would have cut the exemption to approximately $7 million has been eliminated, removing the urgency to use the exemption before a deadline.

• Even with higher exemptions, proactive planning around asset appreciation, portability elections, and gifting strategies remains important for Raleigh professionals with growing estates.

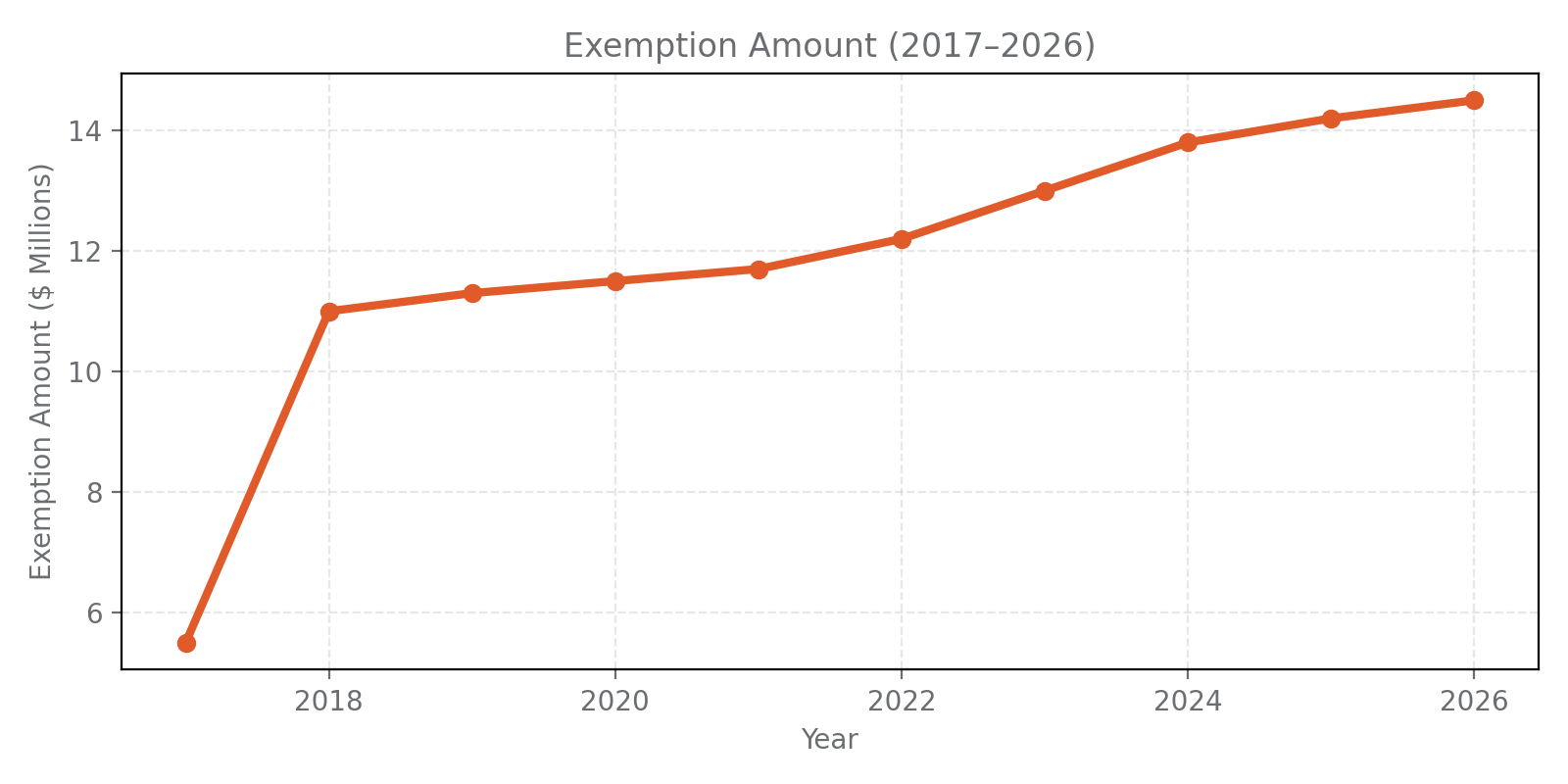

Timeline showing federal estate tax exemption changes from 2017 TCJA through 2026 OBBBA

What is the federal estate tax exemption in 2026 and how does it affect Raleigh high earners?

The federal estate tax exemption for 2026 is $15 million per individual and $30 million for married couples who elect portability. Estates below these thresholds owe no federal estate tax.

• The $15 million exemption was established by the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, which raised the baseline from the TCJA’s $10 million (inflation-adjusted) and removed the scheduled sunset provision.

• The exemption will be indexed for inflation beginning in 2027, meaning the threshold will increase annually without requiring new legislation.

• Estates exceeding the exemption are taxed at a maximum federal rate of 40% on the amount above the threshold.

Portability is not automatic. The surviving spouse must file IRS Form 706 (federal estate tax return) after the first spouse’s death to claim the deceased spouse’s unused exemption, even if the estate falls below the filing threshold.

According to the IRS tax year 2026 inflation adjustments, published October 9, 2025 (Revenue Procedure 2025-32).

Those numbers matter, but here’s what they mean in practical terms for your family.

Let me be very clear with you: even though $15 million sounds like a number that doesn’t apply to most people, your estate may be closer to that threshold than you think. When you add up the equity in your home, your retirement accounts, life insurance death benefits, business interests, and investment portfolios, the total grows quickly. A dual-income couple in Raleigh with a medical practice, a home in North Hills, two 401(k)s, and a $2 million life insurance policy could be looking at a combined estate value of $8 million to $12 million today. Factor in 10 to 15 years of growth, and you’re approaching the exemption.

So the question isn’t whether the current exemption applies to you right now. The question is whether your estate will grow into it over the next decade. And quite candidly, for most high-income professionals in the Triangle, the answer is yes.

For a definition of the federal estate tax exemption and how it works, see our federal estate tax exemption glossary page.

Do high income earners in Raleigh, North Carolina owe state estate tax?

No. North Carolina does not impose a state estate tax or inheritance tax. The state’s estate tax was repealed effective January 1, 2013, under Session Laws 2013-316.

• North Carolina is one of 38 states with no estate tax, making it more favorable for high-net-worth estate planning than states like Massachusetts (which has a $2 million state exemption) or New York ($6.94 million in 2025).

• The repeal applies to estates of all decedents dying on or after January 1, 2013, regardless of estate value.

• North Carolina also has no state gift tax, so lifetime gifting strategies face only federal gift tax rules.

If a North Carolina resident owns real property in a state that imposes its own estate or inheritance tax, that state’s tax may still apply to the property located within its borders.

According to North Carolina Session Laws 2013-316, Section 7(a), which repealed NCGS §105-32.1 through §105-32.8, effective January 1, 2013.

This is actually one of the most misunderstood points in estate planning for North Carolina families.

I want to share something with you that comes up in almost every initial consultation we have with high-income clients. They walk in thinking North Carolina has an estate tax. It doesn’t. It hasn’t since 2013. And quite candidly, that’s one of the most significant planning advantages you have as a North Carolina resident.

Here’s what this means for you practically: the only estate tax threshold you need to worry about is the federal $15 million exemption. If you’re married and you plan properly, that’s $30 million protected. Compare that to a colleague in Connecticut or Oregon who faces a state estate tax kicking in at $2 million to $4 million on top of the federal tax, and you can see why North Carolina is a genuinely favorable place to build and protect wealth.

But that doesn’t mean you can ignore planning. The absence of a state estate tax is a reason to plan smarter, not a reason to skip planning entirely.

How will the 2026 federal estate tax changes affect Raleigh high income earners?

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, raised the federal estate and gift tax exemption to a $15 million per-person baseline with no scheduled sunset, removing the TCJA sunset provision that would have reduced the exemption to approximately $7 million per individual in 2026. The generation-skipping transfer (GST) tax exemption also increased to $15 million. Beginning in 2027, all three exemptions will be indexed annually for inflation, as confirmed in IRS Revenue Procedure 2025-32.

So what does this actually change for your planning strategy?

Before the OBBBA, the entire estate planning conversation for high earners was dominated by one question: should I use my exemption before the sunset? Attorneys across the country were pushing clients to make large irrevocable gifts before January 1, 2026, to lock in the higher exemption. That urgency is gone.

But here’s what most people don’t understand: the elimination of the sunset doesn’t mean you should stop planning. It means you can plan more strategically.

Let’s say you’re a 48-year-old surgeon in Raleigh with a combined household estate of $6 million today. At a conservative 6% annual growth rate, your estate reaches $15 million in roughly 15 years. Without planning, your heirs could face a 40% tax on every dollar above the exemption. The math is pretty simple: $1 million over the exemption means $400,000 in federal estate tax. $5 million over means $2 million.

I want to strongly encourage you to use this new stability to your advantage. The pressure to act before a deadline is gone, but the value of acting early is not. Gifting strategies, irrevocable trusts, and retirement account planning all become more effective the earlier you start, because you’re moving assets and their future appreciation out of your taxable estate.

According to the IRS announcement on tax year 2026 adjustments, as of October 9, 2025.

For a detailed look at how irrevocable trusts can help manage estate tax exposure, see trusts for high income earners in North Carolina.

What happens if the exemption drops in the future?

Under the OBBBA, the $15 million federal estate tax exemption has no scheduled sunset provision. However, future legislation could reduce or modify the exemption at any time, as no tax law is immune from congressional action.

• The IRS anti-clawback regulation (Treasury Regulation §20.2010-1(c)) confirms that gifts made under a higher exemption will not be retroactively taxed if the exemption is later reduced by new legislation.

• The exemption will be indexed for inflation starting in 2027, so the threshold is expected to increase gradually each year absent legislative changes.

• State-level estate taxes in other jurisdictions are not affected by the OBBBA and could change independently.

The anti-clawback protection applies to completed gifts. It does not protect assets still held in your estate at death if the exemption has been reduced before that date.

According to Treasury Regulation §20.2010-1(c), which addresses the treatment of gifts made during periods with higher exemption amounts.

This is where the planning gets interesting for high earners who want to protect wealth across generations.

Here’s what I tell every client who asks this question: the fact that the exemption now has no scheduled sunset does not mean it’s guaranteed forever. Congress can change tax law at any time. What the OBBBA gives you is stability and time to plan without a deadline hanging over your head.

And quite candidly, that’s actually better for most families than the old system. Under the old rules, people were making large irrevocable gifts under pressure, sometimes transferring more than they were comfortable parting with, because they were afraid of losing the higher exemption. Now you can take a measured approach. You can gift strategically over time, move appreciated assets into trusts when the timing makes sense, and build a plan that fits your actual financial picture rather than racing a legislative clock.

I want to strongly encourage you to think of the current moment as an opportunity to plan well, not a reason to delay planning indefinitely. The anti-clawback rule means that gifts you make now are protected even if the law changes later. That’s a meaningful safety net.

For strategies on structuring retirement accounts and beneficiary designations within this planning framework, see retirement accounts and SECURE Act planning for Raleigh professionals.

Frequently asked questions

Does the $15 million exemption apply to each spouse separately?

Yes. Each individual has a $15 million exemption in 2026. Married couples can protect up to $30 million combined if the surviving spouse files IRS Form 706 to elect portability of the deceased spouse’s unused exemption.

According to IRC §2010(c)(4), which governs the portability election for deceased spousal unused exclusion amounts.

Is the annual gift tax exclusion the same as the lifetime exemption?

No. The annual gift tax exclusion ($19,000 per recipient in 2026) is separate from the $15 million lifetime exemption. You can give $19,000 per person per year without filing a gift tax return or reducing your lifetime exemption. Gifts above $19,000 per recipient require a gift tax return and reduce your available lifetime exemption.

According to IRS tax year 2026 inflation adjustments, as of October 9, 2025.

Do I need to file a federal estate tax return if my estate is under $15 million?

Not necessarily for tax purposes, but yes if your spouse dies first and you want to preserve their unused exemption through portability. The portability election requires filing Form 706, even when no tax is owed. Failing to file means the deceased spouse’s unused exemption is lost permanently.

According to IRS Form 706 instructions.

The federal estate tax picture for 2026 is clearer than it has been in years. The exemption is $15 million, it has no scheduled sunset, and North Carolina adds no state estate tax on top of it. But clarity doesn’t mean simplicity. Your estate is growing, your retirement accounts have beneficiary designations that may be outdated, and the SECURE Act changed how your heirs will receive those accounts.

I want to strongly encourage you to use this stability as your starting point, not your stopping point. If we can be of assistance to you in building or updating your estate plan, please schedule a free discovery call or reach out to us at 919-647-9599.

About the Author

Jason Walls, J.D., is the Founder and Chief Legal Officer of The Walls Law Group, a North Carolina law firm focused on helping business owners and families protect, preserve, and transfer wealth through estate, business, and asset protection planning.

This content was reviewed on March 17th, 2026.

Disclaimer: This page is for educational purposes only and does not constitute legal or tax advice. The information provided is general in nature and may not apply to your specific situation. Estate planning, tax planning, and trust administration involve complex legal and financial considerations that vary based on individual circumstances. For specific legal advice tailored to your circumstances, please schedule a consultation with a qualified estate planning attorney. Tax laws are subject to change, and the information on this page reflects the law as of February 2026.