Retirement accounts and SECURE Act planning for Raleigh high income earners

For most high-income professionals in Raleigh, retirement accounts represent the single largest asset in their estate. A physician with 20 years of 401(k) contributions, a tech executive with a deferred compensation plan, a business owner with a SEP-IRA. These accounts often hold $500,000 to $3 million or more, and the way they transfer to your heirs changed dramatically when the SECURE Act eliminated the stretch IRA in 2020.

This page explains exactly what the SECURE Act and SECURE 2.0 Act changed, how the 10-year distribution rule works, and what Raleigh high earners should be doing right now to minimize the tax impact on their families.

On this page:

• What did the SECURE Act change for retirement account inheritance?

• How does the 10-year rule work for inherited retirement accounts?

• Why is the 10-year rule especially costly for high income beneficiaries?

• Beneficiary designation strategies for Raleigh high earners

• Should high income earners consider Roth conversions?

• When should a trust be named as a retirement account beneficiary?

• Frequently asked questions

At a glance:

• The SECURE Act of 2019 eliminated the stretch IRA for most non-spouse beneficiaries, replacing it with a mandatory 10-year distribution rule.

• Non-spouse beneficiaries who inherit a traditional IRA or 401(k) must withdraw the entire account balance within 10 years of the original owner’s death, and those withdrawals are taxed as ordinary income.

• For a Raleigh professional earning $300,000 or more whose adult children inherit a $1 million IRA, the 10-year rule can push those children into higher tax brackets and result in $200,000 to $350,000 in combined federal and state income taxes on the inherited account.

• Strategic Roth conversions, beneficiary designation reviews, and trust-based planning can significantly reduce the tax burden on inherited retirement accounts.

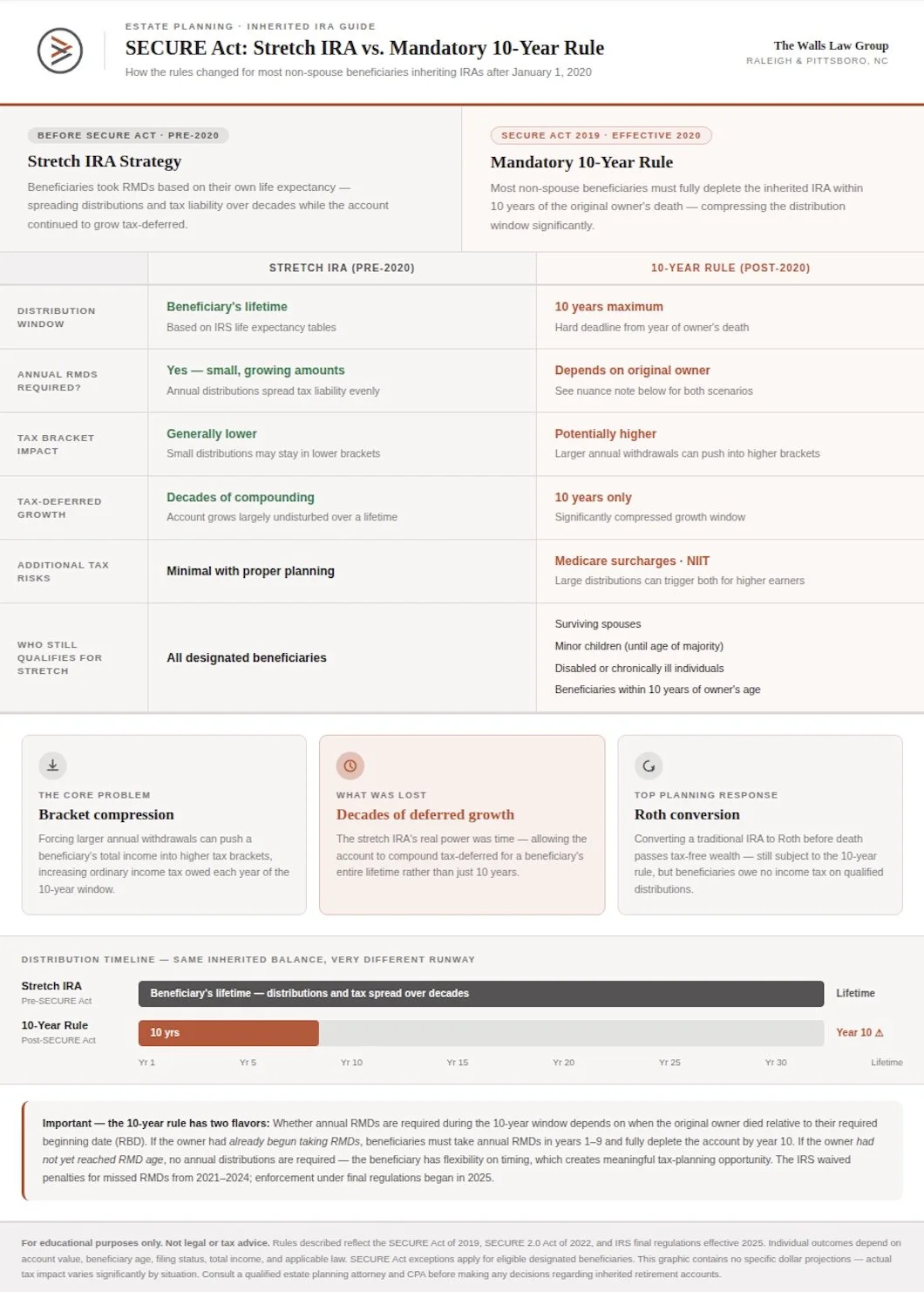

Stretch IRA versus SECURE Act 10-year rule comparison showing accelerated tax impact on inherited retirement accounts.

What did the SECURE Act change for retirement account inheritance?

The Setting Every Community Up for Retirement Enhancement Act (SECURE Act), enacted December 20, 2019, eliminated the "stretch IRA" strategy for most non-spouse beneficiaries of inherited retirement accounts. Before the SECURE Act, a non-spouse beneficiary could distribute an inherited IRA or 401(k) over their own life expectancy, potentially stretching tax-deferred growth across 30 to 50 years. The SECURE Act replaced this with a mandatory 10-year distribution window for most non-spouse beneficiaries.

• 10-year rule. Most non-spouse beneficiaries (including adult children) who inherit a retirement account from an account owner who dies after December 31, 2019, must withdraw the entire account balance by the end of the 10th year following the year of death.

• Eligible designated beneficiaries (exceptions). Five categories of beneficiaries are exempt from the 10-year rule and can still use the stretch: surviving spouses, minor children of the account owner (until they reach the age of majority, then the 10-year clock starts), disabled individuals, chronically ill individuals, and beneficiaries who are not more than 10 years younger than the account owner.

• SECURE 2.0 Act updates (2022). The SECURE 2.0 Act raised the required minimum distribution (RMD) age to 73 (effective 2023) and to 75 (effective 2033), expanded Roth employer contribution options, and increased catch-up contribution limits for ages 60 to 63.

• IRS final regulations (July 2024). The IRS clarified that for inherited accounts from owners who had already begun RMDs, non-spouse beneficiaries must take annual distributions during the 10-year window (not just empty the account by year 10). For accounts from owners who had not begun RMDs, beneficiaries have flexibility in the timing of distributions as long as the account is fully distributed by the end of year 10.

According to the SECURE Act (Pub. L. 116-94, Division O), Section 401, and IRS final regulations on the 10-year distribution rule published July 2024.

The mechanics of the 10-year rule are straightforward. The tax consequences are where it gets complicated.

Here’s what most people don’t realize about this change: the stretch IRA was one of the most powerful wealth-transfer tools available to families. A 35-year-old who inherited a $1 million IRA could stretch distributions over 48 years, taking out roughly $20,000 to $25,000 per year while the remaining balance continued to grow tax-deferred. The annual tax hit was manageable, and the compounding effect was extraordinary.

The SECURE Act compressed all of that into 10 years. Same $1 million. Same income tax on every dollar that comes out. But now your beneficiary has to take it in one decade instead of five. And quite candidly, for high-income families in Raleigh, that compression creates a tax problem that most people haven’t planned for.

How does the 10-year rule work for inherited retirement accounts?

Under the SECURE Act 10-year rule, a non-spouse beneficiary who inherits a traditional IRA, 401(k), 403(b), or similar tax-deferred retirement account must withdraw the entire account balance by December 31 of the 10th year following the year of the original account owner’s death. The distributions are taxed as ordinary income in the year withdrawn.

• No required annual distribution (in most cases). If the original account owner died before their required beginning date for RMDs, the beneficiary can choose when to take distributions during the 10-year window. They could take nothing for 9 years and withdraw everything in year 10, though this would create a massive taxable event.

• Annual distributions may be required. If the original account owner had already begun taking RMDs before death, the IRS final regulations (July 2024) require the beneficiary to take annual distributions during the 10-year period based on the beneficiary’s life expectancy, with the remaining balance fully distributed by the end of year 10.

• Inherited Roth accounts. The 10-year rule also applies to inherited Roth IRAs and Roth 401(k)s. However, because Roth distributions are generally tax-free (assuming the account has been open for at least 5 years), the tax impact is minimal. The account must still be emptied by year 10, but the beneficiary owes no income tax on the withdrawals.

According to the SECURE Act, Section 401, and IRS guidance on inherited retirement account distributions.

The flexibility in timing sounds helpful until you see what happens to the tax bill.

Let me walk you through the math with a real scenario. You’re a 60-year-old cardiologist in Raleigh with a $1.5 million traditional 401(k). You pass away. Your two adult children, both in their early 30s and earning $150,000 each, inherit the account equally. Each child receives $750,000.

Under the old stretch rules, each child could have taken roughly $15,000 to $18,000 per year for the rest of their lives. At a 24% marginal rate, that’s $3,600 to $4,300 per year in taxes. Manageable.

Under the 10-year rule, each child needs to withdraw $75,000 per year (on average) over 10 years. That $75,000 per year gets stacked on top of their existing $150,000 income, pushing them into the 32% bracket and potentially into the 35% bracket in peak distribution years. Over 10 years, each child could pay $180,000 to $250,000 in federal and North Carolina income taxes on the inherited account. Combined, your family gives up $360,000 to $500,000 of the $1.5 million to taxes.

I want to strongly encourage you to look at your retirement accounts through this lens. The balance you see on your statement is not the amount your family will receive. The after-tax inheritance is what matters.

Why is the 10-year rule especially costly for high income beneficiaries?

The 10-year distribution rule creates the largest tax impact when the beneficiary is already in a high income tax bracket. Because inherited IRA and 401(k) distributions are taxed as ordinary income, the required distributions stack on top of the beneficiary’s existing earnings and can push them into progressively higher federal brackets.

• A beneficiary earning $200,000 per year who takes a $100,000 inherited IRA distribution will be taxed on $300,000 of total income, with the distribution taxed at the 32% to 35% marginal rate.

• North Carolina imposes a flat state income tax of 3.99% (as of 2026) on all taxable income, adding to the federal burden on every inherited dollar.

• The net investment income tax (NIIT) of 3.8% may also apply to beneficiaries with modified adjusted gross income exceeding $200,000 (single) or $250,000 (married filing jointly), depending on the composition of their income.

• The combined effective tax rate on inherited retirement account distributions for a high-income Raleigh beneficiary can reach 37% to 42% when federal, state, and NIIT are combined.

This is where planning shifts from optional to essential.

And quite candidly, this is the piece that keeps me up at night for our high-income clients. The SECURE Act didn’t just change the timeline. It changed who gets taxed the hardest. If your children are successful professionals themselves, earning $200,000 to $400,000, they’re exactly the people who get hit the worst by the 10-year rule. Every dollar from the inherited account stacks on top of their already high income and gets taxed at the highest marginal rates.

Compare that to a beneficiary earning $50,000. Their inherited distributions push them from the 22% bracket into maybe the 24% bracket. The tax impact is real but proportionally much smaller.

The irony is that the families who worked hardest to save in tax-deferred accounts are the ones whose children face the steepest tax bills on the inheritance. That’s not a reason to stop contributing to your 401(k). It’s a reason to plan the distribution strategy before your family has to deal with it.

Beneficiary designation strategies for Raleigh high earners

Beneficiary designations on retirement accounts override the instructions in a will or trust. This means the person or entity named on the beneficiary form at your 401(k) provider or IRA custodian controls who receives the account at death, regardless of what your estate plan says. Reviewing and updating beneficiary designations is one of the most impactful and least expensive estate planning actions a high earner can take.

• Name individuals, not your estate. Naming your estate as the beneficiary of a retirement account eliminates all stretch and 10-year rule benefits. The account must be distributed within 5 years (if the owner died before the required beginning date) or over the owner’s remaining life expectancy, often resulting in a faster and larger taxable distribution.

• Review after life changes. Beneficiary designations should be reviewed after every marriage, divorce, birth, death, or significant change in financial circumstances. An outdated designation naming an ex-spouse can override your current will and trust.

• Consider per stirpes designations. Naming beneficiaries "per stirpes" ensures that if a named beneficiary predeceases you, their share passes to their own children rather than being redistributed among the surviving beneficiaries.

• Coordinate with your estate plan. Beneficiary designations should be reviewed alongside your will, trust, and overall estate plan to ensure consistency. A $2 million life insurance policy going to one child while a $2 million IRA goes to another may seem equal on the surface, but the after-tax values are dramatically different.

Spousal beneficiaries have unique options unavailable to non-spouse beneficiaries. A surviving spouse can roll the inherited account into their own IRA, delay distributions until their own RMD age, and name new beneficiaries. This is almost always the most tax-efficient option for the surviving spouse.

According to IRS guidance on retirement plan beneficiary designations and SECURE Act Section 401 provisions on eligible designated beneficiaries.

Getting the designations right is the first step. The second step is reducing the tax burden before you pass.

Let me be very clear with you: I see beneficiary designation errors more often than any other estate planning mistake. A client comes in with a beautifully drafted trust, a comprehensive will, and a clear distribution plan. Then we pull the beneficiary forms on their retirement accounts and discover the 401(k) still names their first spouse from 15 years ago. Or the IRA lists their estate as the beneficiary because that’s what the default form said when they opened the account in 2008.

These are not hypothetical problems. I see them in initial consultations every single month. And the consequences are severe. A beneficiary designation that names your estate instead of your children can cost your family tens of thousands of dollars in unnecessary taxes and eliminate the 10-year distribution option entirely.

I want to strongly encourage you to pull every beneficiary form you have. Your 401(k), your IRA, your life insurance, your annuities if you have them. Read the names on those forms. If anything is outdated, incorrect, or names your estate, fix it this week. It costs nothing and it may be the single most valuable thing you do for your family.

Should high income earners consider Roth conversions?

A Roth conversion involves moving funds from a traditional IRA or 401(k) into a Roth IRA. The converted amount is taxed as ordinary income in the year of conversion, but all future growth and qualified distributions from the Roth account are tax-free. For high-income earners concerned about the SECURE Act’s impact on their heirs, Roth conversions can shift the tax burden from the beneficiaries to the account owner during their lifetime, when the tax rate may be more manageable.

• Tax-free inheritance. Inherited Roth IRAs are still subject to the 10-year distribution rule, but the distributions are tax-free (assuming the 5-year holding period has been met). A $1 million inherited Roth IRA delivers $1 million to your beneficiaries. A $1 million inherited traditional IRA may deliver only $600,000 to $700,000 after taxes.

• No RMDs during your lifetime. Roth IRAs have no required minimum distributions during the owner’s lifetime, allowing the account to continue growing tax-free for as long as you live.

• Strategic timing. The ideal time for Roth conversions is during years when your income is lower than usual: the year after retirement but before RMDs begin, a sabbatical year, or a year with large deductible expenses. Converting during a lower-income year means paying tax at a lower marginal rate.

• Partial conversions. You don’t have to convert the entire account in one year. Converting $100,000 to $200,000 per year over 5 to 10 years can keep you within a targeted tax bracket and avoid pushing into the 37% rate.

Roth conversions are not always beneficial. If you expect your beneficiaries to be in a significantly lower tax bracket than you, the math may favor leaving the account as a traditional IRA and letting them pay tax at their lower rate. This analysis requires comparing your current marginal rate, your projected rate in retirement, and your beneficiaries’ expected rates.

According to IRS guidance on Roth IRA conversions and distributions.

The Roth conversion decision intersects with another important question: should a trust be involved?

Here’s the way I explain Roth conversions to clients. You are prepaying your family’s tax bill at today’s rate so they don’t have to pay it at tomorrow’s rate. Whether that’s a good deal depends on the numbers.

Let me give you a specific example. You’re a 55-year-old attorney in Raleigh earning $400,000 per year. You have $1.2 million in a traditional IRA. You plan to retire at 62 and start Social Security at 67. Between ages 62 and 67, your income drops dramatically. Those are your conversion years. You convert $150,000 per year for 5 years, paying tax at the 24% to 32% bracket instead of the 35% to 37% bracket your children would face.

By the time you’re 67, you’ve moved $750,000 into a Roth IRA. Your children inherit that account and take distributions over 10 years, tax-free. The remaining $450,000 in the traditional IRA still goes through the 10-year rule, but the tax exposure is cut by more than half.

And quite candidly, for clients with estates approaching the federal exemption, there’s a second benefit: paying the conversion tax reduces the size of your taxable estate. The tax payment itself is a form of wealth transfer.

When should a trust be named as a retirement account beneficiary?

Naming a trust as the beneficiary of a retirement account adds complexity and should only be done when specific planning goals require it. A trust beneficiary designation can provide control over how and when distributions are made to beneficiaries, protect inherited assets from creditors or divorce, and manage distributions for minor children or beneficiaries with special needs.

• Conduit trust. A conduit trust requires the trustee to pass all retirement account distributions through to the trust beneficiary in the year received. The distributions are taxed at the beneficiary’s individual rate rather than the compressed trust tax brackets. This works well when the goal is creditor protection without additional tax cost.

• Accumulation trust. An accumulation trust allows the trustee to retain distributions inside the trust rather than passing them through to beneficiaries. This provides maximum control but triggers trust income tax rates, which reach the top 37% bracket at just $16,000 of income (2026). This is typically used only for special needs planning or situations requiring strict asset protection.

• See-through trust requirements. For a trust to qualify for the 10-year rule (rather than the less favorable 5-year rule), it must meet the IRS "see-through" requirements: the trust must be valid under state law, become irrevocable at death, have identifiable beneficiaries, and the trust document must be provided to the account custodian by October 31 of the year following death.

In most cases, naming individual beneficiaries directly on the account is simpler, less expensive, and more tax-efficient than using a trust. A trust should only be the beneficiary when the control or protection benefits outweigh the additional cost and complexity.

According to IRS requirements for trust beneficiaries of retirement accounts and Treasury Regulation §1.401(a)(9)-4 (see-through trust requirements).

This decision sits at the intersection of tax planning, estate planning, and family dynamics.

I want to share something with you that I emphasize with every client who asks about naming a trust as their IRA beneficiary: do not do it unless there is a specific reason. The default answer should be to name your spouse as primary beneficiary and your children individually as contingent beneficiaries.

The specific reasons that justify a trust beneficiary include minor children (you need someone to manage the money until they’re old enough), a beneficiary with a disability or special needs (where an inheritance could disqualify them from government benefits), a beneficiary with creditor or divorce risk, or a beneficiary who cannot manage money responsibly.

If none of those apply, naming individuals directly gives your family the most tax-efficient outcome. The last thing you want is your $1 million IRA trapped inside an accumulation trust, paying 37% federal tax on every dollar above $16,000. That’s a planning mistake, not a planning strategy.

For how trusts work in North Carolina and when each type makes sense, see trusts for high income earners in Raleigh. For how the federal estate tax exemption interacts with retirement account planning, see federal estate tax and the 2026 changes.

Frequently asked questions

Does the 10-year rule apply to inherited Roth IRAs?

Yes. Non-spouse beneficiaries must still withdraw the entire balance of an inherited Roth IRA within 10 years. However, because Roth distributions are tax-free (assuming the 5-year holding period is met), there is no income tax impact. The 10-year rule for inherited Roth accounts is a timing rule, not a tax event.

Can my surviving spouse roll my 401(k) into their own IRA?

Yes. A surviving spouse is the only beneficiary who can roll an inherited 401(k) or IRA into their own retirement account, treat it as their own, delay distributions until their own RMD age, and name new beneficiaries. This spousal rollover is almost always the most tax-efficient option and should be the default strategy unless there is a specific reason to disclaim or use a trust.

What happens if I name my estate as the beneficiary?

Naming your estate as the retirement account beneficiary is one of the most costly mistakes in estate planning. It eliminates the 10-year distribution option, forces distributions under less favorable rules (typically 5 years if you die before your required beginning date), makes the account subject to probate and creditor claims, and can result in significantly higher taxes. Always name individual beneficiaries or a properly structured trust.

Should I stop contributing to my 401(k) because of the SECURE Act?

No. The tax-deferred growth during your lifetime still provides substantial benefits, and employer matching contributions are essentially free money. The SECURE Act changes how the account is distributed after your death, but it does not reduce the value of contributing during your working years. The planning adjustment is to develop a distribution and conversion strategy alongside your contribution strategy, not to stop contributing.

How often should I review my beneficiary designations?

Review beneficiary designations annually and after every major life event: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in financial circumstances. Beneficiary designations override your will and trust, so even a perfectly drafted estate plan can be undermined by an outdated form naming the wrong person.

Your retirement accounts are likely the largest or second-largest asset in your estate, and the SECURE Act fundamentally changed how they transfer to your family. The 10-year rule is not going away. The question is whether you plan around it or let it cost your family hundreds of thousands of dollars in avoidable taxes.

If we can be of assistance to you in reviewing your beneficiary designations, evaluating a Roth conversion strategy, or coordinating your retirement accounts with your overall estate plan, please schedule a free discovery call or reach out to us at 919-647-9599.

About the Author

Jason Walls, J.D., is the Founder and Chief Legal Officer of The Walls Law Group, a North Carolina law firm focused on helping business owners and families protect, preserve, and transfer wealth through estate, business, and asset protection planning.

This content was reviewed on March 17th, 2026

Disclaimer: This page is for educational purposes only and does not constitute legal, tax, or financial advice. The information provided is general in nature and may not apply to your specific situation. Retirement account planning, Roth conversions, and beneficiary designation strategies involve complex legal, tax, and financial considerations that vary based on individual circumstances. For specific advice tailored to your circumstances, please consult with a qualified estate planning attorney and a tax professional. Tax laws are subject to change, and the information on this page reflects the law as of February 2026.