Trusts for high income earners in North Carolina: when you need one and which type fits

If you’re earning $300,000 or more per year in Raleigh and your estate is growing, the question isn’t whether you need a trust. The question is which type of trust matches your goals and at what point the benefits justify the setup.

This page breaks down the two primary categories of trusts used by high-income North Carolina professionals, explains when each one makes sense, and gives you the specific dollar thresholds and scenarios where the planning starts to pay for itself. Everything here is grounded in North Carolina’s Uniform Trust Code (NCGS Chapter 36C), which governs how trusts are created, managed, and modified in this state.

On this page:

• When does a high income earner in Raleigh need a trust?

• Revocable living trusts: what they do and who they’re for

• Irrevocable trusts: when asset protection and tax reduction matter

• How North Carolina trust law affects your planning

• Side-by-side: revocable vs irrevocable trust for Raleigh professionals

• Frequently asked questions

At a glance:

• A revocable living trust is the foundation of most high-income estate plans. It avoids probate, maintains privacy, and gives you full control during your lifetime.

• An irrevocable trust becomes relevant when your estate approaches the federal exemption threshold ($15 million individual, $30 million married in 2026), when you face professional liability exposure, or when you want to remove appreciating assets from your taxable estate.

• North Carolina’s Uniform Trust Code (NCGS Chapter 36C) provides flexibility to modify even irrevocable trusts through consent, judicial modification, or decanting.

• The single most common trust mistake is creating a revocable trust and failing to retitle assets into it. An unfunded trust provides no probate avoidance.

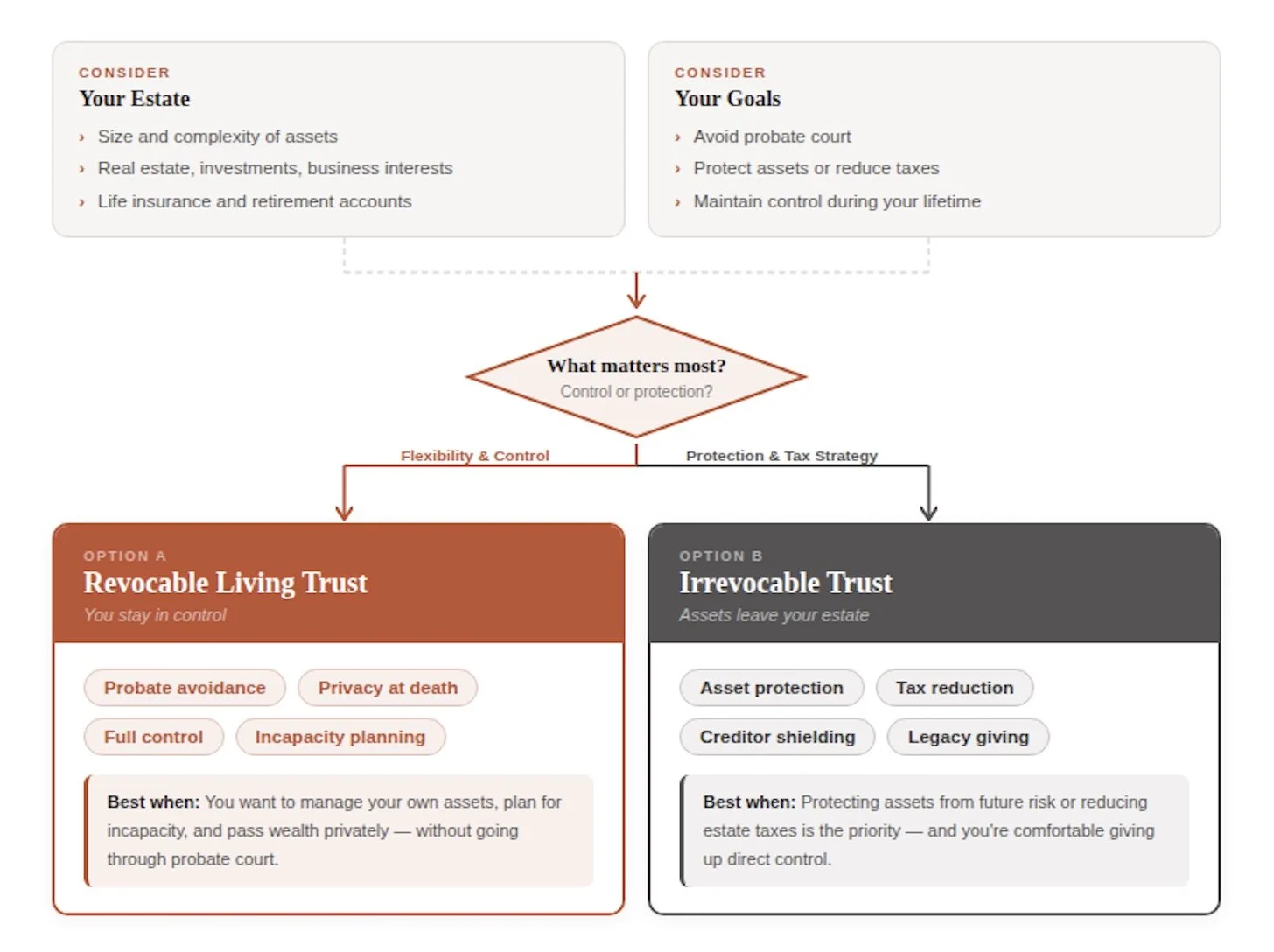

Trust selection decision tree for Raleigh high income earners comparing revocable and irrevocable trust benefits.

When does a high income earner in Raleigh need a trust?

A trust becomes a practical necessity for North Carolina residents when the estate includes assets that would otherwise go through probate, when financial privacy is a priority, or when the combined estate value creates potential federal estate tax exposure. There is no minimum net worth required to create a trust, but the benefits become most pronounced for individuals and families with estates exceeding $1 million in total value.

• If you own real property in your individual name, that property will go through probate at death unless it is titled in a trust or held in joint tenancy with right of survivorship.

• If you have minor children, a trust allows you to name a trustee to manage assets on their behalf rather than relying on a court-supervised guardianship.

• If you are a physician, attorney, business owner, or other professional with liability exposure, certain trust structures can shield assets from future creditor claims.

• If your combined estate (home equity, retirement accounts, life insurance, investments, business interests) exceeds $5 million and is growing, you should be evaluating whether irrevocable trust strategies make sense alongside a revocable living trust.

According to NCGS Chapter 36C (North Carolina Uniform Trust Code), which governs the creation and administration of all trusts in North Carolina.

The first trust most high earners should consider is the revocable living trust. Here’s why.

Let me be very clear with you: the conversation about trusts is not about your income. It’s about your assets. I work with clients who earn $350,000 per year but have relatively modest estates because they’re early in their careers. I also work with clients who earn less but have accumulated $3 million to $5 million in home equity, retirement savings, and business value over 20 years.

The threshold I use as a starting point is $1 million in total estate value. At that level, probate costs, delays, and the public nature of the process become significant enough that a revocable living trust starts to make financial sense. By the time your estate reaches $3 million to $5 million, the trust is no longer optional. It’s the foundation of the entire plan. And once you’re approaching $7 million to $10 million, we need to be having a more advanced conversation about irrevocable strategies.

Revocable living trusts: what they do and who they’re for

A revocable living trust is a legal arrangement where you (the grantor) transfer assets into a trust that you control during your lifetime. You serve as the initial trustee, retain full authority to amend or revoke the trust, and continue to use the assets as your own. At your death, the successor trustee you named distributes assets to your beneficiaries according to the trust terms, without probate.

• Probate avoidance. Assets titled in the trust bypass the Wake County probate process entirely. There is no court filing, no three-month creditor period, and no public record of what was distributed or to whom.

• Privacy. Unlike a will, which becomes public record when filed with the Clerk of Superior Court, a trust is a private document. The terms, the asset values, and the beneficiaries remain confidential.

• Incapacity planning. If you become incapacitated, the successor trustee steps in to manage trust assets immediately, without the need for a court-appointed guardianship or conservatorship.

• Control. You decide exactly how and when assets are distributed. You can set age-based distributions for children (for example, one-third at age 25, one-third at 30, and one-third at 35), create incentive provisions, or require that assets remain in trust for a beneficiary’s lifetime.

A revocable trust does not provide asset protection from creditors during the grantor’s lifetime. Under NCGS §36C-5-505, creditors can reach assets in a revocable trust to satisfy the grantor’s debts. It also does not reduce estate taxes, because the assets remain part of your taxable estate.

According to NCGS Chapter 36C, Article 6 (Revocable Trusts), §36C-6-602 (capacity to revoke) and §36C-5-505 (creditor access).

So if a revocable trust doesn’t protect assets or reduce taxes, when do you need an irrevocable trust?

I want to share something with you that surprises most of our clients: the revocable living trust is not about taxes. At all. It’s about control, privacy, and avoiding the probate process for your family.

Here’s the scenario I see most often in Raleigh: a married couple, both professionals, with a home worth $600,000 to $900,000, two retirement accounts, a brokerage account, and a life insurance policy. Total estate value is somewhere in the $2 million to $4 million range. They’re nowhere near the $15 million federal exemption. Estate taxes are not their issue.

Their issue is what happens when one of them passes away. Without a trust, the surviving spouse has to open a probate case for every asset titled in the deceased spouse’s name alone. With a trust, the surviving spouse calls the successor trustee (often themselves), and the assets continue without interruption. No court. No waiting. No public filings.

And quite candidly, for families with young children, the control provisions alone justify the trust. You can make sure your children don’t receive a $500,000 inheritance at age 18 with no guardrails.

Irrevocable trusts: when asset protection and tax reduction matter

An irrevocable trust is a legal arrangement where the grantor permanently transfers assets out of their personal ownership and into the trust. Once funded, the grantor generally cannot amend, revoke, or reclaim the transferred assets. In exchange for giving up control, the assets are removed from the grantor’s taxable estate and shielded from the grantor’s creditors.

• Estate tax reduction. Assets transferred to an irrevocable trust, along with all future appreciation on those assets, are excluded from the grantor’s taxable estate. For estates approaching the $15 million federal exemption, this can eliminate or significantly reduce federal estate tax exposure.

• Creditor and liability protection. Unlike revocable trusts, properly structured irrevocable trusts are generally beyond the reach of the grantor’s creditors. For physicians, attorneys, and business owners with professional liability exposure, this is a critical planning tool.

• Generation-skipping planning. Irrevocable trusts can be designed as dynasty trusts or generation-skipping trusts to benefit multiple generations while minimizing transfer taxes at each generational level. The GST tax exemption is also $15 million per individual in 2026.

• Life insurance trust (ILIT). An irrevocable life insurance trust holds a life insurance policy outside the grantor’s estate, so the death benefit is not subject to estate tax. For a high earner with a $2 million to $5 million life insurance policy, an ILIT can save $800,000 to $2 million in federal estate taxes.

The trade-off is control. Once assets are in an irrevocable trust, you cannot take them back. You cannot change the terms without the consent of all beneficiaries (NCGS §36C-4-411), a court order (NCGS §36C-4-412), or through a decanting action. North Carolina does allow trust decanting, which provides more flexibility than many states, but it’s not a simple process.

According to NCGS Chapter 36C, Articles 4 and 5, governing trust modification (§36C-4-411, §36C-4-412) and creditor’s claims (§36C-5-505).

The question every high earner should ask is: at what point does the loss of control justify the tax and protection benefits?

Here’s how I think about the irrevocable trust conversation with clients. If your estate is under $5 million, we are almost certainly focused on a revocable living trust and proper beneficiary designations. You don’t have a federal estate tax problem, and the flexibility of the revocable trust is more valuable to you than the protection of an irrevocable one.

When your estate reaches the $5 million to $10 million range, we start looking at specific irrevocable strategies for specific assets. A life insurance policy with a $3 million death benefit? That belongs in an ILIT. A rapidly appreciating business interest? Moving a portion into an irrevocable trust now, while the value is lower, captures all the future growth outside your estate.

And once your estate exceeds $10 million to $15 million, the irrevocable trust is no longer optional. At that point, every dollar above the exemption is taxed at 40%. The math is straightforward: $1 million over the exemption costs your family $400,000 in federal estate taxes. $5 million over costs $2 million. I want to strongly encourage you to run these numbers with your estate planning attorney and your financial advisor together, because the decisions you make now about which assets to move into irrevocable structures will compound over the next 10 to 20 years.

How North Carolina trust law affects your planning

North Carolina adopted the Uniform Trust Code in 2005 (NCGS Chapter 36C), which provides a comprehensive statutory framework for creating, administering, and modifying trusts. Several provisions of NC trust law are particularly relevant for high-income estate planning.

• Modification by consent (NCGS §36C-4-411). A trust can be modified or terminated by consent of the settlor and all beneficiaries, even if the modification is inconsistent with the original trust purpose. This provides an escape valve for irrevocable trusts when circumstances change.

• Judicial modification (NCGS §36C-4-412). A court can modify a trust if its purposes have been fulfilled or are no longer achievable, or if circumstances have changed in ways the settlor did not anticipate. The court must consider the trust’s purpose and the interests of all beneficiaries.

• Trust decanting. North Carolina allows a trustee with discretionary distribution authority to “decant” trust assets from one irrevocable trust into a new trust with different terms. This is one of the most powerful tools in NC trust law for adapting irrevocable trusts to changed circumstances without court involvement.

• Creditor access to revocable trusts (NCGS §36C-5-505). During the grantor’s lifetime, assets in a revocable trust are fully accessible to the grantor’s creditors. After death, creditors may reach trust assets to the extent they could have reached the grantor’s probate estate. This is why a revocable trust alone does not provide asset protection.

• Spendthrift provisions. North Carolina recognizes spendthrift clauses in irrevocable trusts, which prevent beneficiaries’ creditors from reaching trust assets before distribution. This is particularly valuable for protecting inherited wealth from a beneficiary’s divorce, lawsuits, or poor financial decisions.

According to NCGS Chapter 36C (North Carolina Uniform Trust Code).

These provisions give North Carolina trust planning more flexibility than many people expect from irrevocable structures.

Here’s what I want you to take away from this section: irrevocable does not mean unchangeable in North Carolina. That surprises a lot of people. The old perception of an irrevocable trust was that once you signed it, you were locked in forever. That’s not how NC law works.

The consent modification provision, the judicial modification option, and especially the decanting power give us tools to adapt your trust as your life changes. Had a new child? We can adjust the trust. Business value changed dramatically? We can restructure. Tax law shifted? We can decant the trust into a new trust that takes advantage of the new rules.

And quite candidly, this flexibility is one of the reasons North Carolina is a favorable state for trust planning. Not every state offers all three of these modification paths.

Side-by-side: revocable vs irrevocable trust for Raleigh professionals

Revocable living trust

• You retain full control and can amend or revoke at any time.

• Assets remain in your taxable estate.

• No creditor protection during your lifetime (NCGS §36C-5-505).

• Avoids probate and maintains privacy.

• Best for estates under $10 million focused on probate avoidance and family control.

• Typical cost to establish: $2,500 to $5,000 for a comprehensive revocable trust package.

Irrevocable trust

• You give up control of transferred assets.

• Assets are removed from your taxable estate (reduces estate tax exposure).

• Provides creditor and liability protection for transferred assets.

• Can include spendthrift provisions to protect beneficiaries.

• Best for estates exceeding $5 million, or for specific assets (life insurance, rapidly appreciating business interests) at any estate level.

• Typical cost to establish: $3,500 to $10,000 depending on the trust type and complexity.

Scenario 1: Dual-income couple, combined estate $2.5 million

You’re both physicians in your late 30s. Your estate includes a $550,000 home, two 401(k)s totaling $600,000, a brokerage account, and a $1 million life insurance policy. Your primary concerns are probate avoidance and making sure your young children are protected. A revocable living trust is the right foundation. The life insurance policy could go into an ILIT if you want to remove the death benefit from your taxable estate, but at this estate level, that’s optional.

Scenario 2: Business owner, combined estate $7 million

You own a dental practice valued at $1.5 million, a home worth $800,000, retirement accounts totaling $1.2 million, and a $3 million brokerage portfolio. Your estate is growing at 6% to 8% annually, which means you could reach the $15 million exemption within 10 to 12 years. A revocable living trust handles probate avoidance. An irrevocable trust should hold the life insurance. And we should be discussing moving a portion of the business interest into an irrevocable structure now, while the value is lower, to capture future appreciation outside your estate.

Scenario 3: Late-career executive, combined estate $12 million

You’re a 58-year-old tech executive with RSUs, a $1.4 million home, substantial retirement savings, and deferred compensation. Your estate will likely exceed the $15 million exemption before you retire. A revocable living trust is the baseline. Irrevocable trusts for life insurance, gifting strategies using the annual exclusion, and potentially a grantor retained annuity trust (GRAT) for the RSUs are all on the table. The planning needs to be coordinated with your financial advisor and CPA because every dollar you move now is a dollar (plus all its growth) that your family keeps instead of paying 40% to the IRS.

For the key differences between these two trust types, see our revocable vs irrevocable trust comparison. For how trusts interact with retirement account planning, see retirement accounts and the SECURE Act.

Frequently asked questions

Can I be the trustee of my own revocable living trust?

Yes. In fact, that’s the standard arrangement. You serve as the initial trustee, maintain full control of all trust assets, and can buy, sell, or manage them as you normally would. You also name a successor trustee who steps in if you become incapacitated or at your death.

Does a revocable trust protect assets from lawsuits?

No. Under NCGS §36C-5-505, assets in a revocable trust are accessible to the grantor’s creditors during the grantor’s lifetime. If you need liability protection for specific assets, an irrevocable trust or other asset protection strategy is required. This is a particularly important distinction for physicians and attorneys in Raleigh who face professional malpractice exposure.

What assets should go into a revocable living trust?

Generally, your primary residence, secondary real property, brokerage and investment accounts, and business interests should be retitled into the trust. Retirement accounts (401(k), IRA) should not be retitled into the trust because doing so triggers a taxable distribution. Instead, you name the trust as the beneficiary of retirement accounts only in specific circumstances, and this requires careful coordination with the SECURE Act’s 10-year distribution rule.

How much does it cost to set up a trust in North Carolina?

A comprehensive revocable living trust package for a high-income family in Raleigh typically costs $2,500 to $5,000 and includes the trust document, pour-over will, durable power of attorney, health care power of attorney, and living will. Irrevocable trusts are typically $3,500 to $10,000 depending on the type and complexity. These costs should be weighed against the potential cost of probate, which can run $5,000 to $15,000 or more for a high-value estate.

Can I change an irrevocable trust after it’s created?

In North Carolina, yes, under certain circumstances. NCGS §36C-4-411 allows modification by consent of the settlor and all beneficiaries. NCGS §36C-4-412 allows judicial modification when circumstances have changed. And North Carolina’s trust decanting provisions allow a trustee with discretionary authority to transfer trust assets into a new trust with updated terms. These options make NC irrevocable trusts more flexible than in many other states.

A trust is not a one-size-fits-all solution. The type of trust you need, the assets you put into it, and the timing of those transfers all depend on your specific financial picture, your family structure, and your goals. For most high-income professionals in Raleigh, the revocable living trust is the foundation. As your estate grows into the $5 million to $15 million range, irrevocable strategies become essential.

If we can be of assistance to you in determining which trust structures fit your situation, please schedule a free discovery call or reach out to us at 919-647-9599.

About the Author

Jason Walls, J.D., is the Founder and Chief Legal Officer of The Walls Law Group, a North Carolina law firm focused on helping business owners and families protect, preserve, and transfer wealth through estate, business, and asset protection planning.

This content was reviewed on March 17th, 2026

Disclaimer: This page is for educational purposes only and does not constitute legal or tax advice. The information provided is general in nature and may not apply to your specific situation. Trust creation and administration involve complex legal and financial considerations that vary based on individual circumstances. For specific legal advice tailored to your circumstances, please schedule a consultation with a qualified estate planning attorney. Laws are subject to change, and the information on this page reflects the law as of February 2026.